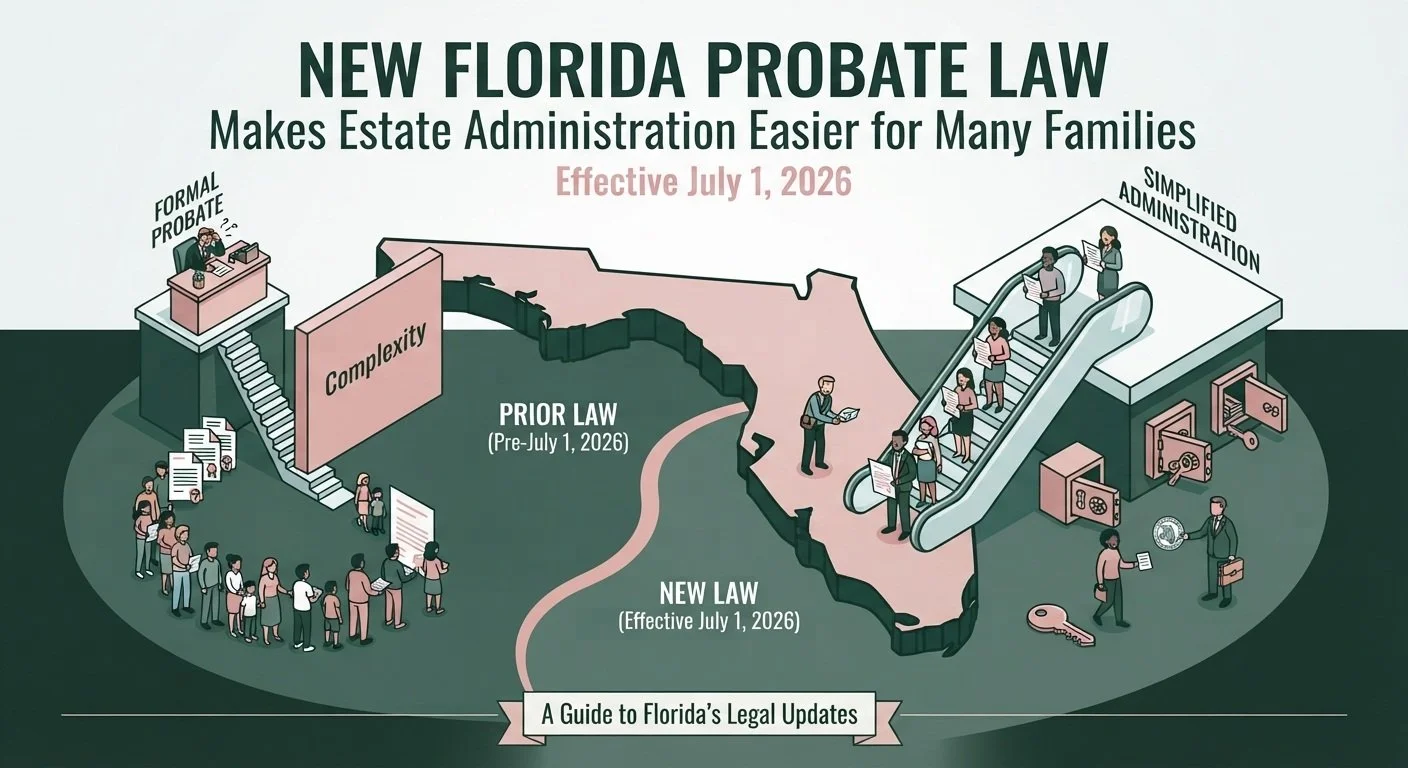

New Florida Probate Law Makes Estate Administration Easier for Many Families

Effective July 1, 2026, Florida has made several important changes to its probate laws that will simplify estate administration for many families and personal representatives.

House Bill 1337 updates…

Why Estate Planning Costs Less Than Probate in Florida

One of the most common reasons people put off estate planning is because they think it's too expensive.

I understand. Creating a will or trust can feel like a significant investment, especially when you're healthy and not thinking about what might happen years down the road.

But here's what many people don't realize:

A Will Isn't Enough to Protect Your Child in a Crisis — Here's What Is

Most parents I talk to assume that if something happened to them, the people they love would step in and take care of their kids. And most of the time, that's true.

But "most of the time" isn't good enough when it comes to your children.

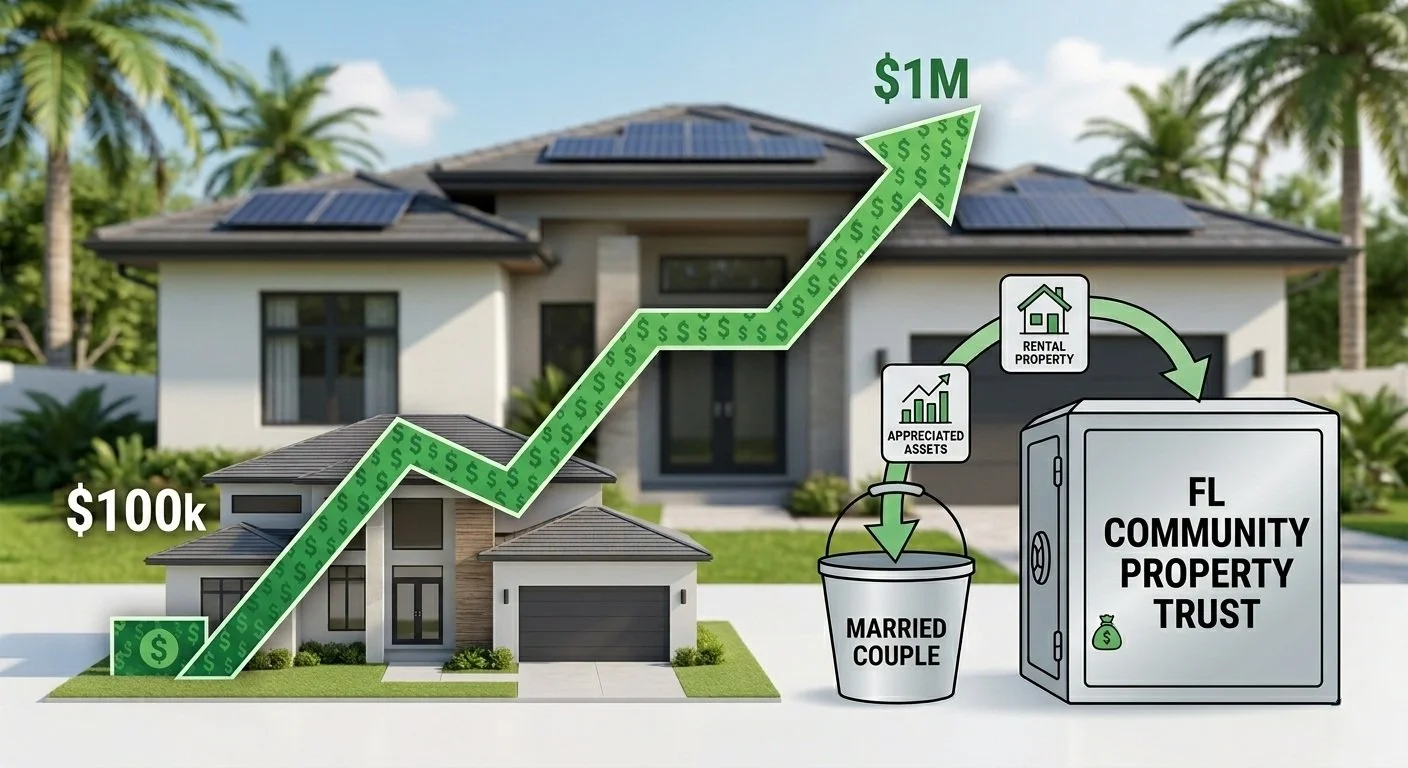

Florida Community Property Trusts: A Powerful Estate Planning Tool for the Right Couple

Many Florida residents are surprised to learn that Florida now allows married couples to create a Community Property Trust (CPT)—an estate planning strategy that may provide significant income tax benefits for highly appreciated assets.

While Florida is not traditionally a community property state, legislation enacted in 2021 allows married couples to voluntarily elect community property treatment for assets transferred into a properly drafted Community Property Trust. For the right family, this can create substantial tax savings and simplify estate planning.

Caring for Aging Parents Without Letting It Divide the Family

Taking care of an aging parent can bring families closer together, but it can also expose cracks that have been there for years. One sibling often becomes the default caregiver. Another handles the finances. Someone else lives out of state and feels disconnected, or criticized for not doing enough. Before long, small disagreements turn into major conflicts.

Unfortunately, this happens more often than most families expect.

Protecting Your Child With Special Needs: What Every Parent Needs to Know

If you have a child with special needs, standard estate planning advice doesn't apply to your family. In fact, following it could seriously backfire.

Here's why.

Why Many Families Are Better Off With a Living Trust

While a will is a vital first step, many Florida families are surprised to learn that it doesn’t avoid probate—it requires it. In this post, we break down why a living trust is often the smarter move for those looking to bypass the 18-month waiting period, avoid heavy court fees, and keep their private affairs off the public record. From understanding the importance of "funding" your trust to planning for incapacity, learn how a mindful approach to estate planning can provide your loved ones with immediate security and peace of mind.

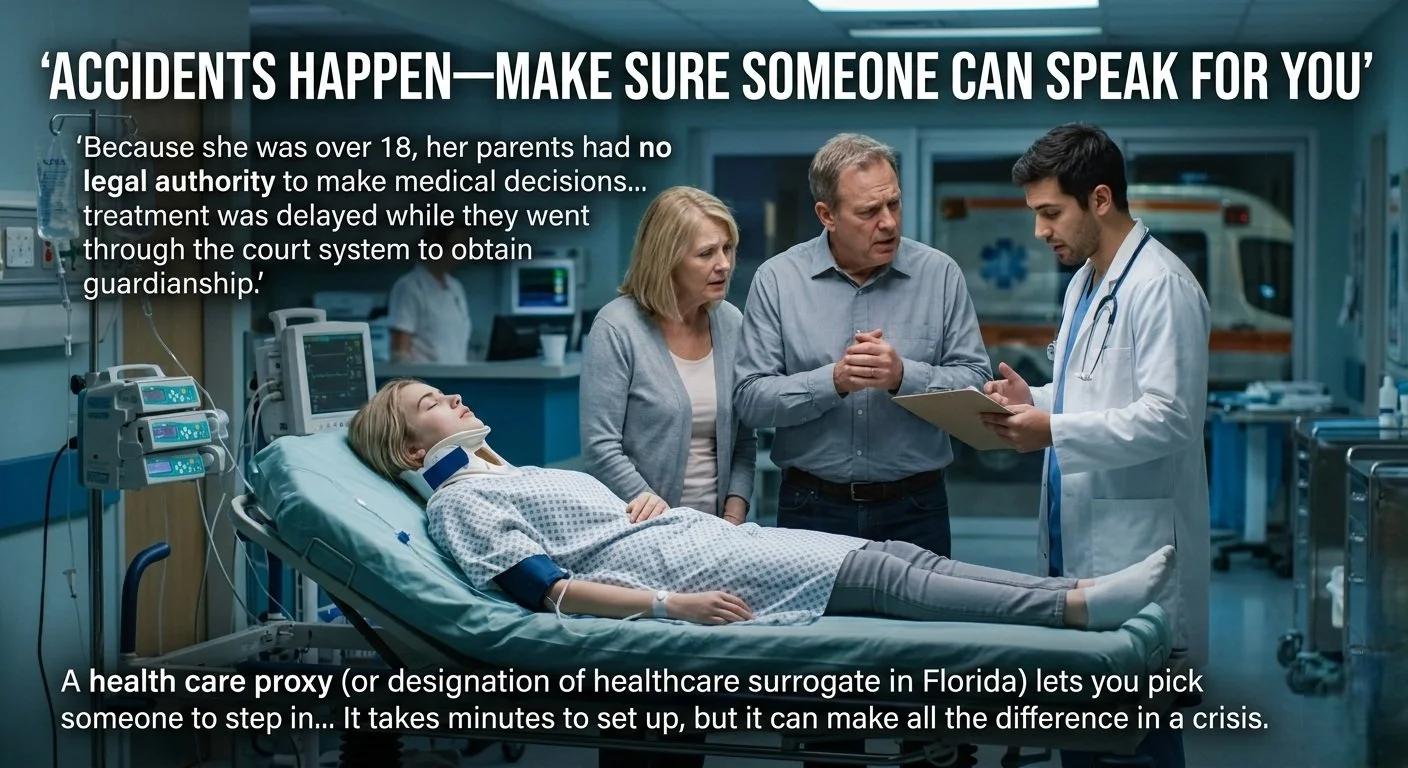

Accidents Happen—Make Sure Someone Can Speak for You

A health care proxy (also known as a “Designation of Healthcare Surrogate, here in Florida) is a legal document that allows you to appoint someone you trust to make medical decisions on your behalf if you become unable to communicate. This person you pick is called your health care agent. They will step in to ensure that doctors follow your wishes regarding treatment, life support, and other medical care.

Why Your LLC Operating Agreement Might Matter More Than Your Will

When families in Central Florida think about estate planning, they usually focus on wills and trusts. Those documents are vital, but if you own a business—especially a Florida LLC—there’s another document that often has the "final say" on what happens to your company when you die: your Operating Agreement.

As a business succession and estate planning attorney, I see many owners in Winter Garden and Windermere who are surprised to learn that their Will does not automatically determine who inherits or runs their company. In fact, Florida courts have consistently held that a well-drafted Operating Agreement acts as a binding contract that can override a Will entirely.

Estate Planning for a Child with Special Needs: Protecting Their Future in 2026

For parents in Central Florida, planning for a child with special needs is a deeply personal mission. You aren’t just planning for "who gets what"—you are building a safety net that must last a lifetime.

In 2026, expanded federal eligibility for ABLE Accounts and new Florida trust rules have changed the landscape. As a Special Needs Planning Attorney, I help families in Winter Garden, Windermere, and Clermont navigate these tools to ensure their child stays protected without losing vital government benefits like SSI and Medicaid.

Common Estate Planning Mistakes That Cost Families More Than They Expect

DIY and low-cost estate planning options can feel like a smart, efficient choice. The documents look professional, everything is signed, and it seems like the job is done.

The problem is that most estate planning mistakes are not obvious. They are structural. And they often aren’t discovered until a family is already dealing with loss.

When reviewing estate plans created online or by attorneys who do not regularly focus on estate planning, the same patterns appear again and again. The intentions are good, but the execution is often wrong or incomplete.

When Your Child Turns 18, Everything Legally Changes

As parents, we spend years making medical and financial decisions for our children without a second thought. We sign permission slips, speak with doctors, manage insurance, and handle paperwork as needed.

But did you know that the moment your child turns 18, that legal authority disappears? Even if your child still lives at home. Even if you still pay their bills. Even if they still call you for advice.

Legally, they are now an adult.

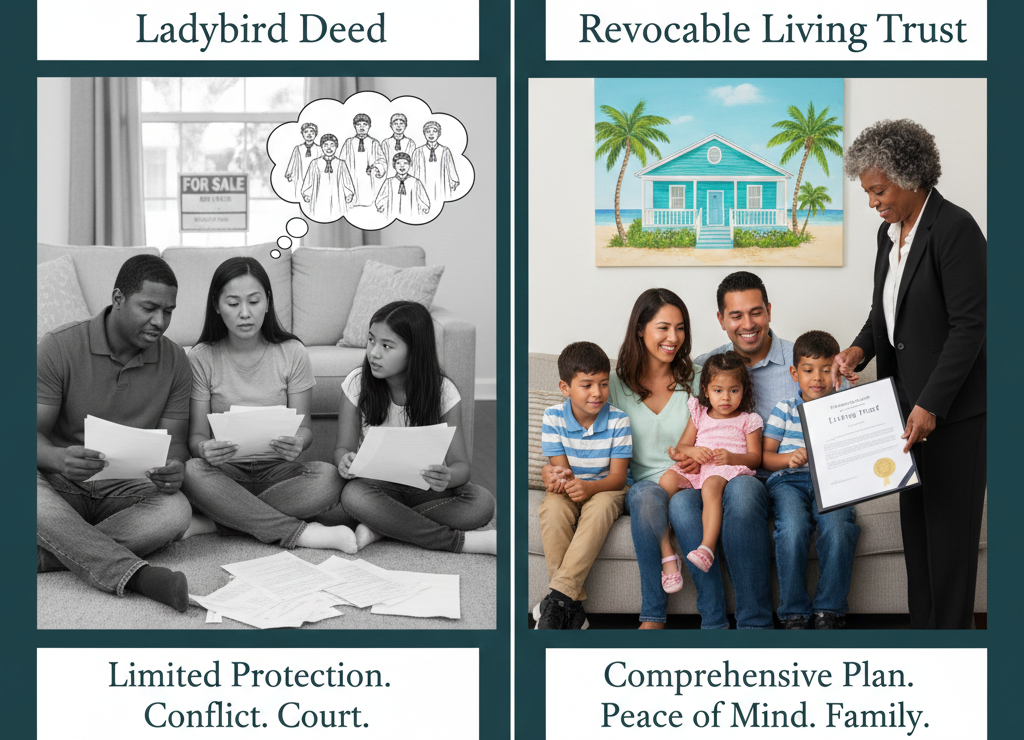

Lady Bird Deed vs. Revocable Living Trust: Protecting Your Florida Home

Most homeowners looking for an Estate Planning Attorney in Central Florida start by asking a single question: "Is a Lady Bird deed a cheaper way to avoid probate?" While families from The Villages to Orlando often consider these deeds a quick, low-cost fix, the reality is that a deed is an isolated document, whereas a Revocable Living Trust is a complete legal strategy. As a Florida attorney serving the high-growth communities of Orange and Lake Counties, I help families determine which tool actually secures their legacy—and which one leaves it vulnerable to the courts.

Why Your "DIY" Online Will Might Be a Gift to a Probate Lawyer

If you search "create a will online," you’ll see dozens of ads promising a "legal document in 15 minutes." While it’s true you can download a template and sign it, there is a massive gap between a valid document and an effective estate plan.

As a legal professional, I’ve seen how "cheap" online wills often become the most expensive mistake a family can make. Before you click "download," here is the reality of what happens when these documents hit a courtroom.

What Happens to Your Debt When You Die and How to Protect Your Family

One of the questions I hear most often is: What happens to my debt when I die? Or, just as often: What happens to my parent’s debt?

The answer is: it depends. And whether that answer causes stress for your family - or peace of mind - comes down to planning.

Debt doesn’t magically disappear

Who Will Take Care of You as You Age? Why Planning Ahead Matters

Many people assume that when they need help later in life, a spouse, child, or close friend will step in. But that assumption is becoming increasingly risky. Today, more than 16 million Americans over age 65 live alone, and most have no formal plan for long-term care or decision-making support as they age.

Can AI Really Draft Your Estate Plan? What Families Need to Know

Artificial intelligence (AI) has made huge strides in the past few years, bringing futuristic technology into our everyday lives. Tools like ChatGPT can already write emails, brainstorm marketing ideas, answer questions, and even help with educational programs. It’s natural to wonder: could AI eventually replace the work of estate planning attorneys? And more importantly, is it safe to trust a computer with something as important as your family’s future?

We decided to put AI to the test by asking ChatGPT

Estate Planning for Military Families: What You Need to Know

Military families live with realities most civilians never have to think about - sudden deployments, frequent moves, unpredictable schedules, and the everyday risks that come with serving our country. Those constant changes make protecting your family especially important, and often a simple, one-page will isn’t enough to cover everything your family may need. Here’s what every military family should know so you can feel confident, prepared, and protected,wherever the military takes you next.

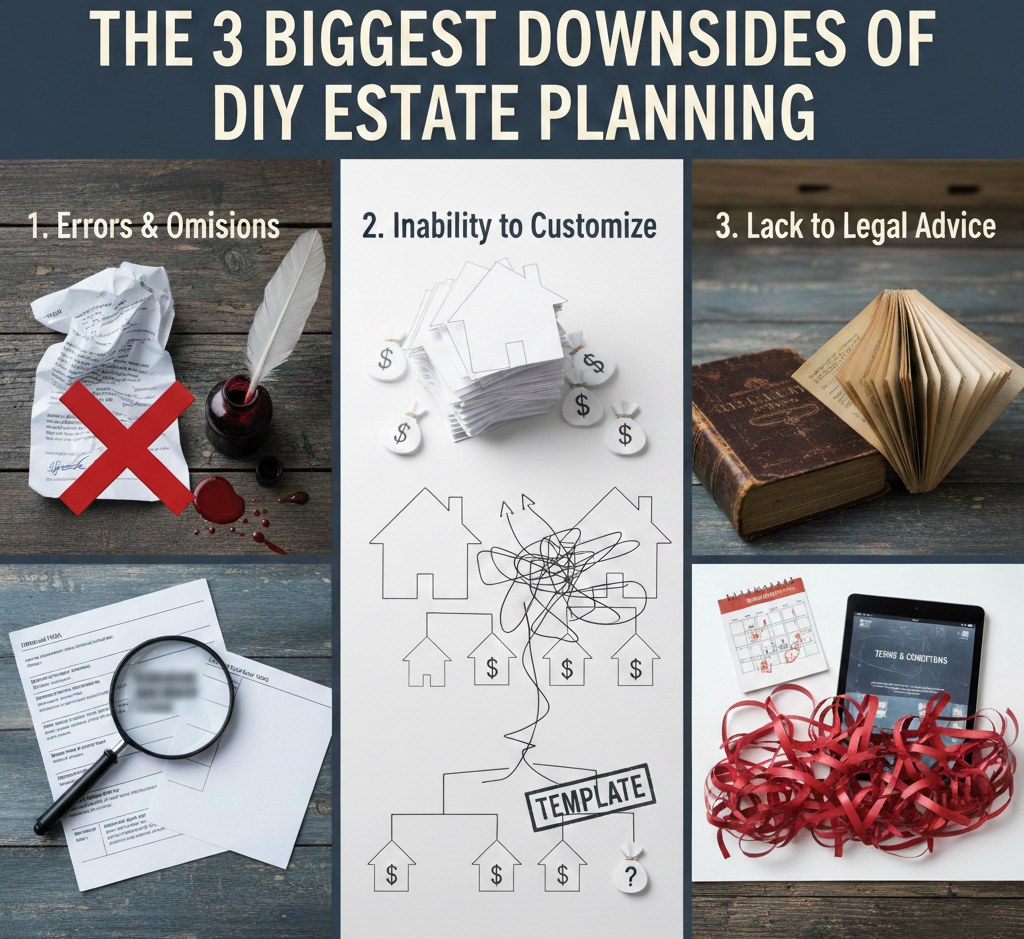

The 3 Biggest Downsides of DIY Estate Planning

With so many online options for creating your own will and estate planning documents, it’s tempting to go the DIY route. While this might seem quick and affordable, there are some major drawbacks to consider. Here are 3 big reasons to think twice before tackling your estate planning alone:

The Estate Tax Is Changing in 2026 — Here’s What That Means for You

Originally Published: Dec 7, 2025 | Latest Update: 2026

🚨 2026 FLASH UPDATE: Since this post was first published, the "Estate Tax Sunset" has been officially repealed by the One Big Beautiful Bill Act (OBBBA). The federal exemption has actually increased to $15 million per person (roughly $30 million for married couples) for 2026. While the "tax cliff" is gone for now, Florida families still face major risks regarding probate, asset growth, and legal formalities. Read below for the original context and how to navigate these new numbers.

There’s a major change coming in estate planning, and it may affect your family without you even realizing it.